What Is the Event in the Headline Most Likely a Response to?

Overview

The outlook for euro expanse activeness and inflation has become very uncertain and depends crucially on how the Russian state of war in Ukraine unfolds, on the impact of current sanctions and on possible farther measures. [one] The baseline includes an initial assessment of the impact of the war on the euro surface area economic system based on the information available up to two March 2022. Soaring energy prices and negative conviction effects imply significant headwinds to domestic demand in the most term, while the appear sanctions and sharp deterioration in the prospects for the Russian economy volition weaken euro area trade growth. The baseline projections are built on the assumptions that current disruptions to free energy supplies and negative impacts on confidence linked to the conflict are temporary and that global supply chains are non significantly affected. Based on these assumptions, the baseline projections foresee a meaning negative impact on euro area growth in 2022, from the conflict. Nonetheless, given the starting point for the euro area economy, with a stiff labour market and headwinds related to the pandemic and supply bottlenecks causeless to fade, economic action is all the same projected to expand at a relatively stiff pace in the coming quarters. Over the medium term, growth is projected to converge towards historical average rates, despite a less supportive fiscal stance and an increase in interest rates in line with the technical assumptions based on fiscal market expectations. Overall, real Gdp growth is projected to average three.7% in 2022, 2.viii% in 2023 and 1.6% in 2024. Compared with the December 2021 Eurosystem staff projections, the outlook for growth has been revised downwards by 0.five per centum points for 2022 attributable mainly to the touch of the Ukraine crisis on energy prices, confidence and merchandise. This downward revision is partly offset by a positive acquit-over effect from upward data revisions for 2021. Growth in 2023 has been revised down by 0.1 percent points, while in 2024 it is unchanged.

Following a series of exceptional energy price shocks, the conflict in Ukraine implies that headline inflation in the baseline is projected to remain at very high levels in the coming months, before easing slowly towards target. It is set to average v.1% in 2022, 2.one% in 2023 and ane.9% in 2024. Well-nigh-term toll pressures have risen significantly, in particular those related to oil and gas commodities. These pressures are assessed to be more lasting than previously expected and to be only partly first past dampening effects on growth from lower confidence and by weaker trade growth related to the disharmonize. Withal, in the absenteeism of further upwards shocks to commodity prices, energy inflation is projected to drop significantly over the projection horizon. In the brusk term, this reject relates to base effects, while the technical assumptions based on futures prices embed a turn down in oil and wholesale gas prices resulting in a negligible contribution from the energy component to headline inflation in 2024. HICP inflation excluding energy and food remains loftier in 2022, at ii.6%, reflecting stronger price dynamics for contact-intensive services, indirect effects from higher energy prices and upward impacts from ongoing supply bottlenecks. Every bit these pressures ease, this measure out of underlying aggrandizement is expected to decrease to 1.viii% in 2023 and then to ascent to 1.9% in 2024, on account of strengthening demand, tightening labour markets and some second-round furnishings on wages, in line with historical regularities. Compared with the December 2021 Eurosystem staff projections, in cumulative terms over the project horizon, headline inflation has been revised upwards substantially, especially in 2022. This upward revision reflects contempo data surprises, higher free energy commodity prices, more persistent upward pressures from supply disruptions and stronger wage growth, as well related to the planned increment in the minimum wage in Germany. The upward revision also takes into business relationship the contempo return of survey-based indicators of medium-term aggrandizement expectations to levels consistent with the ECB's inflation target. These furnishings more than commencement the negative touch on on inflation of a significant upwards revision to the market-based assumptions on involvement rates and the negative need-related effects of the conflict in Ukraine.

On business relationship of the meaning uncertainty surrounding the impact of the conflict in Ukraine on the euro area economy, in addition to the baseline, ii scenarios accept been prepared. Compared with the baseline, an "agin" scenario assumes that stricter sanctions are imposed on Russia, leading to some disruptions in global value chains. Persistent cuts in Russian gas supplies would lead to higher energy costs and to cuts in euro area production, only this would exist simply temporary every bit substitution into other energy sources takes place. In add-on, geopolitical tensions would exist more sustained than in the baseline, leading to additional financial disruptions and more than persistent uncertainty. Under such a scenario, euro area GDP growth would be i.2 percent points lower than the baseline in 2022, while inflation would be 0.8 percentage points higher. Differences would be more limited in 2023. In 2024, growth would be somewhat stronger than the baseline as the economy catches up subsequently the larger negative touch on economic activity in 2022 and 2023. As oil and gas markets rebalance, the large spikes in energy prices would gradually unwind, causing inflation to refuse below the baseline, especially in 2024. A more "severe" scenario includes, in add-on to the features of the adverse scenario, a stronger reaction of energy prices to more stringent cuts in supply, stronger repricing in financial markets and larger second-round furnishings from rising energy prices. This scenario would imply Gross domestic product growth in 2022 that is 1.4 percentage points below the baseline, while inflation would be 2.0 percentage points college. Significantly lower growth and higher inflation, compared with the baseline, would also exist seen in 2023. Higher persistence of the disruptions triggered by the war imply that, in 2024, the grab-up furnishings on growth would be relatively modest whereas stronger second-round effects would offset the negative impact on inflation from declining free energy prices.

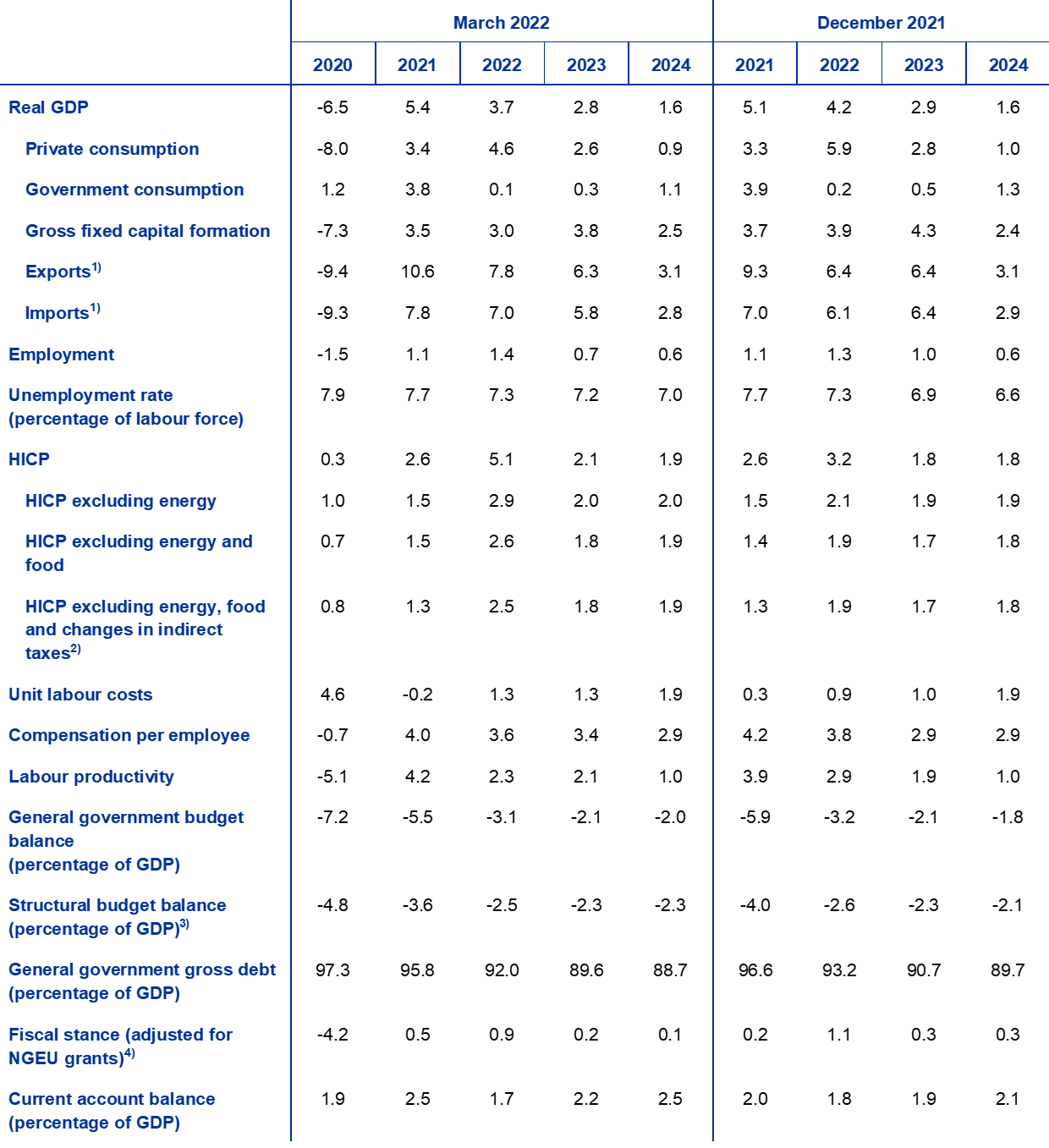

Growth and inflation projections for the euro area

(annual percent changes)

Notes: Real GDP figures refer to seasonally and working day-adjusted data. Historical data may differ from the latest Eurostat publications due to information releases after the cut-off appointment for the projections.

i Existent economy

Real Gross domestic product growth moderated to 0.3% in the fourth quarter of 2021 among tightening supply bottlenecks, more than stringent pandemic restrictions and college energy prices, broadly in line with expectations in the Dec 2021 projections. Private consumption contracted every bit a result of rising infection rates and renewed pandemic uncertainty, coupled with a price-induced drop in real disposable income. In dissimilarity, investment and public consumption provided positive contributions to growth, and economic activity returned to its pre-pandemic level.

Chart i

Euro area existent Gross domestic product growth

(quarter-on-quarter percentage changes, seasonally and working day-adjusted quarterly data)

Notes: Data are seasonally and working day-adapted. Historical data may differ from the latest Eurostat publications due to information releases later the cut-off date for the projections. The vertical line indicates the start of the projection horizon.

Existent GDP growth is expected to remain subdued in the kickoff quarter of 2022 amid tighter mobility restrictions, persistent supply disruptions, high energy prices and the conflict in Ukraine (Chart one). A drop in retail sales in December 2021 (downward two.vii% from November) and a contraction in contact-intensive services due to tighter mobility restrictions at the plough of year translated into a negative deport-over event for growth in the first quarter of 2022. This event appears to have been partially compensated by a marginal monthly increase of retail sales in January 2022 (0.2%). More forward-looking indicators, such equally the composite output Purchasing Managers' Index (PMI) and the European Committee'southward Economic Sentiment Indicator, broadly remained in Jan and Feb at levels seen in the fourth quarter. Despite an improvement in the PMI for manufacturing supplier delivery times in January and February, the alphabetize continues to betoken intense supply disruptions. However, the surveys on which these indicators are based were conducted earlier the outbreak of the disharmonize in Ukraine. Taking the further energy shock and the uncertainty acquired past the Russian invasion of Ukraine also into account, real Gross domestic product growth for the first quarter of 2022 has been revised down by 0.2 percentage points compared to the December projections, and is at present expected to be 0.2%.

The outlook for euro area activity has go very uncertain and crucially dependant on events in Ukraine. The state of war in Ukraine is weakening the near-term growth outlook mainly via trade, commodity prices and confidence channels. Sanctions and the economic drag on the Russian economic system are weighing on euro expanse strange need, even though direct trade linkages with Russia are limited. Soaring energy prices and negative confidence furnishings, coupled with a deterioration in take a chance sentiment and declines in stock prices, imply subdued domestic demand. Nevertheless, our baseline projections assume that any disruption to energy supplies related to the conflict will exist temporary and have no significant lasting affect on economic activeness in the euro area. Box 3 provides more detail on the impact that the disharmonize is expected to accept on the euro area economy and describes two alternative scenarios based on more than negative assumptions.

Economic growth is still projected to pick up from the second quarter of 2022 equally a number of headwinds first to fade, simply this increment is tempered past the negative effects of the conflict in Ukraine. The expected improvement across the almost term is based on a number of supporting factors: a diminishing economical affect from the pandemic, a gradual unwinding of supply bottlenecks and an improvement in export cost competitiveness vis-à-vis key trading partners. In contrast, the disharmonize in Ukraine is expected to negatively affect euro expanse growth. Although the Next Generation European union (NGEU) plan is expected to boost investment in some countries, the withdrawal of temporary government support measures implies that fiscal policy is expected to be less supportive, especially in 2022. Despite the increment in interest rates embedded in the technical assumptions, financing conditions will continue to exist favourable. Overall, despite the downgraded outlook in the short term, real Gdp is foreseen to broadly return to the path expected in the pre-pandemic projections (Chart 2).

Chart 2

Euro area real Gdp

(chain-linked volumes, Q4 2019 = 100)

Notes: Data are seasonally and working day-adjusted. Historical information may differ from the latest Eurostat publications due to information releases afterwards the cut-off date for the projections. The vertical line indicates the showtime of the current projection horizon.

Table 1

Macroeconomic projections for the euro surface area

(annual per centum changes)

Notes: Real Gdp and components, unit labour costs, bounty per employee and labour productivity refer to seasonally and working day-adjusted data. Historical information may differ from the latest Eurostat publications due to information releases after the cut-off date for the projections.

1) This includes intra-euro area merchandise.

2) The sub-alphabetize is based on estimates of actual impacts of indirect taxes. This may differ from Eurostat data, which assume a full and immediate pass-through of indirect revenue enhancement impacts to the HICP.

3) Calculated as the government balance cyberspace of transitory effects of the economic cycle and measures classified under the European System of Central Banks definition as temporary.

4) The fiscal policy stance is measured as the change in the cyclically adjusted primary residue net of government support to the fiscal sector. The figures shown are as well adapted for expected Next Generation European union (NGEU) grants on the revenue side. A negative figure implies a loosening of the fiscal opinion.

Private consumption is projected to recover in the course of 2022, despite the increased uncertainty due to the disharmonize in Ukraine, and to remain the principal driver of growth over the horizon. Against the backdrop of tighter pandemic-related restrictions – especially in contact-intensive services – and rising energy prices, private consumption contracted more than than expected in the fourth quarter of 2021 and stood 2.5% beneath its pre-pandemic level. The higher free energy prices weighing heavily on households' purchasing power besides implies a likely contraction in private consumption in the outset quarter of 2022. Thereafter, private consumption is projected to increment, albeit more moderately than previously expected, reflecting some precautionary saving and further energy toll rises due to the state of war in Ukraine. The selection-upwardly in private consumption is based on the assumptions of a gradual resolution of the pandemic, an easing of supply constraints for consumer goods and only a temporary disruption to energy supplies equally a event of the conflict in Ukraine. Consumption should proceed to outstrip the path of real income in 2023 owing to a further unwinding of savings accumulated since early 2020.

Strong labour income is supporting growth in existent disposable income, while higher inflation rates and the withdrawal of financial transfers are acting as a drag. Existent disposable income is expected to decline strongly in the offset quarter of 2022 on the back of higher aggrandizement and lower net fiscal transfers. A rebound is foreseen from the 2nd quarter of the yr, shaped by improving labour markets and, to a lesser extent, other personal income, in line with moderate growth in economic activity. In contrast, cyberspace financial transfers are expected to weigh on income growth in 2022 every bit the number of people in job retention schemes decreases – with workers mostly transitioning back to regular employment – and other temporary pandemic-related fiscal measures expire. This is partly offset by new measures aimed at compensating for the impact of high energy prices. High inflation is dampening real disposable income more than strongly than previously expected, thus contributing to its refuse in 2022.

The household saving ratio is projected to decline to below its pre-crunch level, before stabilising towards the end of the projection horizon. The saving ratio is expected to fall throughout 2022, revised slightly downwardly since the previous projections. While the conflict in Ukraine raises dubiousness, which would typically be expected to atomic number 82 to an increase in precautionary savings, this issue is more than offset by households' apply of savings to absorber, at least partially, the negative effects of the energy shock on real consumption growth. The normalisation of consumers' saving behaviour reflects the relaxation of containment measures and a dissipation of pandemic-related precautionary motives. The saving ratio is projected to broadly stabilise below its historical average level as of mid-2023. The persistent, albeit slight, undershooting of its historical boilerplate reflects the partial unwinding of excess household savings that have accumulated since the start of the pandemic. However, this result is attenuated past the uncertainty caused by the events in Ukraine and past the concentration of excess savings in wealthier and older households with a lower propensity to consume, while households in the lower income groups remain more exposed to the energy cost shock, also in the light of their lower buffers.[2]

Box one

Technical assumptions about interest rates, commodity prices and substitution rates

Compared with the December 2021 projections, the technical assumptions include significantly college oil and not-oil energy prices and college interest rates. The technical assumptions about interest rates and article prices are based on market expectations with a cutting-off date of 28 February 2022.[iii] Short-term interest rates refer to the 3-month EURIBOR, with market expectations derived from futures rates. The methodology gives an average level for these brusk-term interest rates of -0.4% in 2022, 0.3% in 2023 and 0.7% in 2024. Market expectations for euro surface area ten-yr nominal authorities bond yields imply an average annual level of 0.8% for 2022, gradually increasing over the projection horizon to 1.1% for 2024.[iv] Compared with the December 2021 projections, market expectations for short-term interest rates have been revised up by effectually x, 50 and 70 basis points for 2022, 2023 and 2024, respectively, on the back of expectations of a global tightening of monetary policy, supported past continued positive inflation surprises. This has too led to an upwardly revision of long-term sovereign bond yields, of effectually 50-threescore basis points, over the projection horizon.

As regards commodity prices, the price of a barrel of Brent crude oil is assumed to rise from USD 71.1 on boilerplate in 2021 to USD 92.half-dozen in 2022, earlier failing to USD 77.2 by 2024. This path implies that, in comparison with the December 2021 projections, oil prices in US dollars are virtually twenty% higher for 2022, 14% higher for 2023 and xi% higher for 2024, on the back of supply issues and the state of war in Ukraine. Since the cut-off date, energy prices take increased significantly. The bear upon of higher energy price assumptions than those included in the baseline projections are reflected in the scenarios presented in Box iii.

The prices of non-energy bolt in US dollars rose strongly in 2021 and are expected to ascent more moderately in 2022 and to decrease slightly in 2023-24. EU Emissions Trading Scheme (ETS) allowances are causeless, based on futures prices, to stand around €83 per tonne over the projection horizon – an upward revision of effectually 11% since the December 2021 projections.

Bilateral exchange rates are assumed to remain unchanged over the project horizon at the average levels prevailing in the iii working days ending on the cutting-off date of 28 February 2022. This implies an boilerplate exchange charge per unit of USD one.12 per euro over the period 2022-24, which is around 1% lower than in the December 2021 projections. The supposition for the effective exchange rate of the euro implies an appreciation of 0.iii% since the December 2021 projections.

Technical assumptions

Housing investment is expected to remain positive in the short term and to moderate over the residual of the projection horizon. Housing investment increased slightly in the quaternary quarter of 2021, broadly in line with expectations in the Dec 2021 projections, with shortages of both labour and raw materials weighing on housing market activeness. Despite the war in Ukraine, housing investment is projected to go along to grow in the brusque term against a backdrop of still notable demand – supported specially by stiff demand from higher-income households – and some tentative signs of easing supply constraints. Later a short catch-upwards phase, in which supply constraints are expected to ease more noticeably, growth in housing investment should moderate over the rest of the projection horizon. Nevertheless, it will keep to be supported by positive Tobin'southward Q furnishings and rising disposable income, while financing conditions will get somewhat less favourable.

Concern investment is expected to increment over the project horizon and to business relationship for an increasing share of real GDP, despite the conflict in Ukraine, as supply bottlenecks ease and NGEU funds are disbursed. After the temporary drop in business investment observed in the third quarter of 2021, mostly caused by supply-side bottlenecks, business investment is estimated to take returned to more dynamic growth in the last quarter of 2021. In the short term, despite the increased uncertainty and fiscal market volatility due to the disharmonize in Ukraine, still loftier business concern confidence and capacity utilisation, as well equally a better assessment of majuscule goods producers' order books, point to sustained positive growth. As the supply disruptions ease, investment is expected to maintain a dynamic growth path, although the commodity price increases, negative confidence effects and trade disruptions related to the conflict are likely to human activity every bit a drag. The positive impact of the NGEU programme and projected turn a profit growth in 2022 and beyond are also expected to provide support to business organization investment over the projection horizon. In addition, higher expenditures related to the decarbonisation of the European economic system will provide an additional boost to business investment in the medium term. As a result, business organization investment should business relationship for an increasing share of real GDP over the project horizon.

Box ii

The international environs

The global economy remains on a robust growth path, although the conflict in Ukraine and, to a bottom extent, the spread of the Omicron coronavirus variant cloud the outlook. At the turn of the year, the spread of the new Omicron variant caused an unprecedented increase in the number of coronavirus (COVID-19) infections worldwide. Every bit bachelor bear witness suggests that the Omicron wave volition be shorter than previous waves, the impact on the global economy is expected to be rather moderate and limited to the beginning quarter of 2022. At the aforementioned time, the Russian invasion of Ukraine is weighing on the global economy. The imposition of substantial financial and trade sanctions on Russia has led to a significant downgrading of the country'south growth outlook over the projection horizon (see Box three). In improver to existence channelled by trade linkages, knock-on furnishings are beingness felt by other countries through higher energy prices, thus further reducing households' disposable incomes, and negative confidence effects, which will weigh on domestic need and merchandise.

Supply bottlenecks remain a headwind to growth, simply recent indicators tentatively suggest some moderate easing since the end of 2021. Global PMI suppliers' delivery times have been improving slightly simply remain fairly tight by historical standards and are still long, while bounding main aircraft congestion remains high. At the same time, given the strong growth in appurtenances trade and car production in contempo months, it appears that supply constraints in some sectors may take passed their top. Overall, supply bottlenecks are causeless to ease gradually in the grade of 2022 and to have fully unwound past 2023 as consumer demand switches back from goods to services and shipping capacity and the supply of semiconductors increase on the back of planned investment. Still, there are risks – specially in the short term – that supply disruptions might intensify once more. This could be the example if People's republic of china sticks to its zero-COVID policy with the more than infectious Omicron variant. Moreover, the war in Ukraine could crusade bottlenecks to worsen, leading to shortages of commodities and critical raw materials, but also impediments in logistics and transportation in view of flight and shipping bans affecting merchandise beyond the region.

Over the medium term, the global economic system is projected to continue its expansionary path, admitting at more moderate rates, among geopolitical tensions and the unwinding of the pandemic-related policy stimulus. In 2021 global growth was underpinned by continued policy support. Still, since the December 2021 projections, growth has been revised upwards owing to a better than expected outturn in the 2nd half of the year, especially in large economies such as People's republic of china and the United States. From 2022 onwards, global real Gross domestic product (excluding the euro expanse) is projected to converge to more moderate growth rates. As well the touch on of the Omicron variant and the Russian invasion of Ukraine, private consumption is expected to remain subdued amid rising inflation. Further ahead, "speed limit" furnishings are expected on account of tighter labour market weather condition, which will be partly counterbalanced by the expected dissipation of supply bottlenecks. Diminishing policy support is besides projected to limit growth over the projection horizon. Faced with stiff inflationary pressures, primal banks in some emerging market economies started to unwind their pandemic-related stimulus in 2021. In 2022, budgetary policy accommodation is already beingness – or is soon expected to be – withdrawn as well beyond advanced economies. Since December 2021 the Bank of England has raised interest rates twice and, in the U.s.a., the Federal Open Market Committee has signalled a shift in its policy stance, hinting at a faster pace of normalisation in US monetary policy than previously expected. Growth is therefore projected to decelerate in the United States, also on account of a smaller than previously assumed fiscal stimulus. Among emerging market place economies, growth is projected to slow in Brazil, attributable mainly to aggressive monetary policy tightening amid ascent inflationary pressures, and Turkey, which has experienced market turmoil related to high policy dubiousness and very high aggrandizement, adversely affecting consumption and investment. While the emergence of new, more aggressive coronavirus variants cannot exist ruled out, the influence of the pandemic on the global outlook is assumed to be gradually diminishing. Compared with the December 2021 projections, real GDP growth has been revised downwardly over the projection horizon (-0.4 percentage points for 2022, -0.three percentage points for 2023 and -0.1 percent points for 2024). In the brusk term, the agin touch on of the above-mentioned factors is partly commencement by a positive conduct-over effect, while further into the projection horizon the downward revision relates to weaker growth in the United States and Russia, likewise every bit in some other large emerging market place economies.

Afterwards buoyant growth in 2021, growth in euro area foreign demand is projected to normalise gradually over the projection horizon. In the second one-half of 2021 global trade turned out stronger than expected, notwithstanding supply chain disruptions, driven by robust developments in emerging Asia (mainly Communist china and India) and, in the fourth quarter, the U.s.a.. Survey information point to rather subdued trade growth at the plow of the year, partly on account of the resurgence of the pandemic, just this is expected to be temporary. For 2022, a positive acquit-over effect more than offsets the weaker dynamics stemming from the revisions to global activity and the adverse effects of the conflict in Ukraine, which results in a significant upward revision to growth in global imports for 2022 compared with the Dec 2021 projections. Euro surface area strange need is unrevised for 2022, since the strong positive carry-over effect is fully offset past weaker trade on account of the conflict in Ukraine, while it is revised downward for 2023 and 2024 (-ane.1 percentage points and -0.3 pct points respectively).

The international environment

(annual per centum changes)

ane) Calculated as a weighted boilerplate of imports.

2) Calculated as a weighted boilerplate of imports of euro expanse trading partners.

The conflict in Ukraine is slowing the recovery in merchandise in the brusque term, although momentum is expected to strengthen later in 2022. Post-obit signs of recovery in euro expanse strange demand at the cease of 2021, the state of war in Ukraine is denting the near-term prospect for euro area exports. Some gains in cost competitiveness and the expected recovery in services merchandise should partly offset the headwinds related to the conflict. As a result, quarterly growth rates in euro area exports take been revised down in 2022. Nevertheless, the almanac growth rate has been revised upwardly, on the back of positive deport-over effects from up revisions in the second half of 2021. On the import side, a curt-term dampening of euro area activity dynamics is probable to result in lower growth rates. Net exports are therefore expected to contribute only mildly to GDP growth in 2022. The curt-term outlook withal remains clouded by pregnant downside risks related to supply chains disruptions caused by shortages of primal inputs from Russia. If the effects of the conflict, supply constraints and pandemic-related restrictions unwind, starting in the second half of 2022, euro area trade volition render to its long-term growth path. Strong increases characterise merchandise deflators following the energy price shock, especially on the import side, and will persist throughout 2022. These are also likely to entail a large deterioration in euro expanse terms of merchandise and the trade residual, which are expected to normalise only from 2023.

The labour market continues to strengthen. Employment grew by 0.five% in the fourth quarter of 2021, with a further pass up in the unemployment rate. Employment is projected to grow farther over the project horizon despite some downward pressures from the increased uncertainty due to the state of war in Ukraine. In addition, the unemployment rate is likely going to be adversely affected in the brusk term, only in annual boilerplate terms information technology is projected to decline to 7.0% by 2024. This decline is driven mainly by the projected strong labour demand in line with the ongoing economic recovery.

Labour productivity growth is projected to decline gradually over the projection horizon towards its long-term average. After a temporary dip related to the deceleration in economic activity, labour productivity is expected to regain momentum as a upshot of stronger economic growth and to normalise gradually thereafter towards its long-term pre-pandemic average. Past the end of the projection horizon, labour productivity (per person employed) is expected to be around 4.6% above its pre-crisis level.

Compared with the December 2021 projections, real Gdp growth has been revised downward past 0.5 percentage points for 2022 and by 0.1 percent points for 2023, and is unrevised for 2024. The downgraded outlook for 2022 largely reflects the bear on of the Ukraine crunch on energy prices, confidence and trade, and is partly commencement by a positive carry-over result from upward data revisions for 2021. In 2023 and 2024, upwards impacts from toll competitiveness gains related to college toll pressures in some key trading partners are broadly offset by college interest charge per unit assumptions and a negative impact of higher energy prices.

Box three

The bear on of the conflict in Ukraine on the euro area economic system in the baseline and two culling scenarios

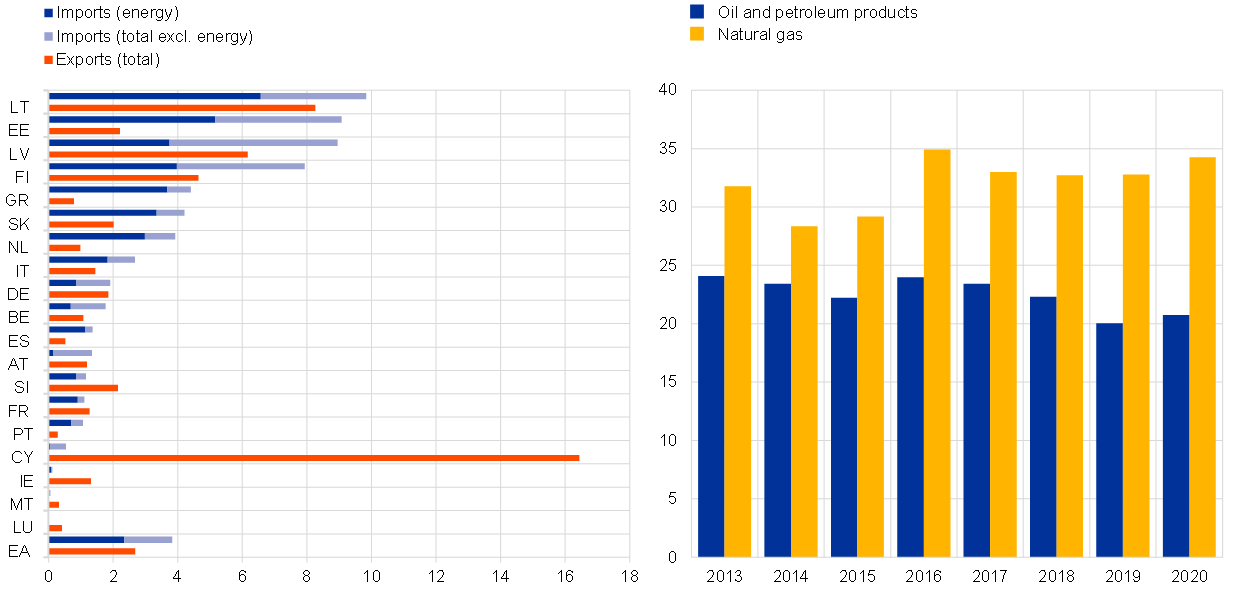

The Russian invasion of Ukraine is expected to significantly touch the euro expanse economy through three main channels: trade, commodities, and confidence. Commencement, merchandise with Russia is afflicted past bans on imports and exports, as well equally the adverse effects of the war on the Russian economic system. The exclusion of Russian banks from SWIFT impairs trade financing of Russian firms, translating into all-encompassing trade disruptions. In addition, a combination of higher interest rates, capital outflows, financing constraints, deterioration of business sentiment, rising import prices and rouble depreciation is weighing on Russian Gdp. While the direct touch on the euro area economy is express, with Russian federation accounting for a small-scale share of euro expanse foreign demand (around 3%; Chart A, left-hand panel), the spillovers to the global economy – notably via countries with stronger trade links with Russian federation, such equally those in cardinal and eastern Europe – weaken the external outlook for the euro area more broadly. 2nd, the outbreak of the conflict has put significant up pressure on commodity prices – already affected by the growing geopolitical tensions in the form of 2021 – across that already embedded in the baseline of the March 2022 projections. The bear upon on the euro area is sizeable, as Russia is its main free energy provider, accounting for 20% of its oil and 35% of its gas in 2020 (Chart A, correct-hand console). While energy sector sanctions take so far been imposed only by non-euro area countries, consumers are increasingly reluctant to buy Russian oil, major companies are divesting Russian oil assets, and banks and insurance companies are increasingly unwilling to finance and insure Russian commodities trade. Finally, the war in Ukraine is eroding global confidence, which in turn is increasing volatility and risk premia in global financial markets. This worsening of financial conditions for euro surface area firms, together with sustained geopolitical tensions and uncertainty, is expected to affect investment.

Nautical chart A

Euro surface area trade with Russia (left-hand console) and euro expanse dependence on Russian free energy supplies (correct-hand panel)

(left-paw panel: percentage of total merchandise in goods and services; right-hand panel: percentage of imports)

Sources: ECB, Eurostat and ECB staff calculations.

Annotation: Imports of natural gas include those of liquefied natural gas.

The loftier uncertainty surrounding the effects of the war in Ukraine on the euro expanse economic outlook warrants additional scenario assay. The baseline projections are congenital on the assumptions that current disruptions to energy supplies and negative impacts on conviction linked to the conflict are temporary and that global supply chains are non significantly affected. Combined with the sanctions and the deterioration in global take a chance sentiment, an energy supply disruption is estimated to weigh on euro area real Gdp growth in 2022 and to hamper activity notwithstanding in 2023, before a small upwards impact in 2024 on account of catch-upwardly effects. As regards HICP aggrandizement, the touch on of the conflict on the baseline of the March 2022 projections is expected to be upwards in 2022 on the back of rising commodity prices but, as the effect progressively fades away, to exist muted in the outer years. This view is based, all the same, on the supposition that the war in Ukraine does not escalate significantly further and that existing sanctions against Russia remain in place over the full projection horizon. Two scenarios (an "agin" scenario and a "severe" scenario) have been synthetic, differing according to sanctions, merchandise, conviction and free energy supply disruptions, merely likewise to the implications of fiscal disruptions and probable reactions. The effects on the euro area are estimated through model-based simulations.[5] It should exist noted that in both alternative scenarios information technology is assumed that the impact of the disharmonize will exist nearly pronounced in 2022 and that in that location will be a resolution of the conflict over time. In this respect, more negative scenarios could exist designed.[half-dozen]

Compared with the March 2022 projections, the adverse scenario assumes a worsening in all three channels (trade, commodities and confidence) and, in particular, constraints in the production capacity of the euro area. On the trade aqueduct, more stringent sanctions entail a more than severe elevate on the Russian economy. These sanctions as well create broad supply constraints and disruptions to global value chains. On the commodity prices aqueduct, the scenario assumes a complete and lengthy cut-off of Russian gas to Europe, which the euro expanse is only able to partly compensate for by using other energy sources and through liquified natural gas substitution. Such a supply shortfall pushes gas prices sharply higher. Similarly, oil supply from Russian federation is severely disrupted, also pushing prices upwards. In addition, the interruption of gas supplies is assumed to trigger cuts in sectoral production across the euro expanse. Besides the energy sector, whose production is directly afflicted, other sectors relying heavily either direct or indirectly on gas (e.g. transportation, mining and quarrying, and chemic products) would be adversely affected as the daze propagates and amplifies downward the supply chain.[vii] Over time, the gas market place is assumed to rebalance, leading to a gradual decline in gas prices and a resumption of product. On the confidence channel, stricter sanctions and more sustained geopolitical tensions than those embedded in the baseline lead to a more severe and protracted rise in global uncertainty and additional financial disruptions that affect some asset categories more than persistently. This in turn further depresses risky nugget prices and increases volatility. Finally, this scenario adds moderate fiscal amplification furnishings attributable to a general increase in chance premia, leading to college external financing costs for euro area firms and weighing on investment.

In improver to the assumptions encapsulated in the adverse scenario, the severe scenario entails a steeper and more than persistent rise in article prices, triggering second-round effects from higher inflation and broader financial amplification effects. In the severe scenario, gas prices are assumed to be twice equally sensitive to Russian gas supplies existence cutting off as in the agin scenario, given the drawdown of inventory stocks and a connected tight gas market place. This entails more severe upwardly price pressures, which are besides expected to be somewhat more persistent considering Russian gas is assumed not to be entirely substitutable over the projection horizon. As a event, the gas market rebalances at more than elevated price levels. In that location is too a sharper increase in oil prices and a higher subsequent price level. On the confidence aqueduct, this scenario assumes larger financial distension effects, with a shock three times the magnitude of that causeless in the adverse scenario. Finally, this scenario includes larger 2nd-round effects in the context of an overall college inflation environment.

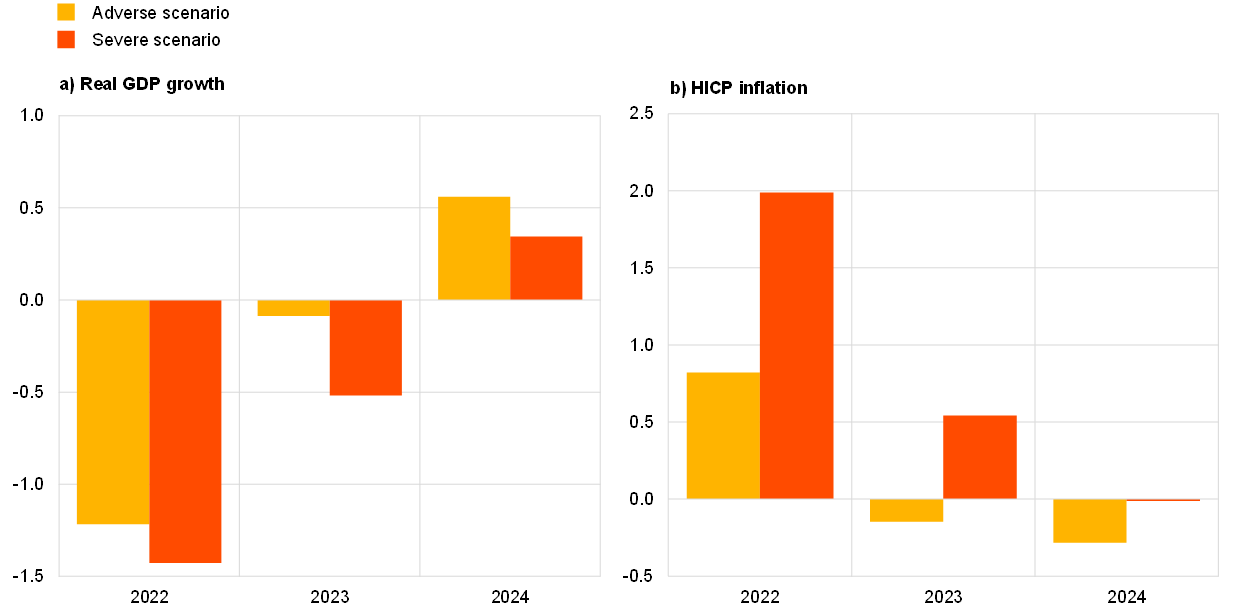

The overall bear on for the euro surface area is significantly negative on existent GDP growth, with a larger and more than persistent event nether the severe scenario (Table and Chart B). In the agin scenario, weaker foreign demand, college commodity prices, heightened uncertainty, repricing in financial markets and production cuts lower real GDP growth past around one.2 percentage points in 2022 and 0.1 pct points in 2023 compared with the baseline. In 2024, growth is 0.5 percentage points higher than the baseline as the economy catches upwards after the larger negative impact on economical action in 2022 and 2023. In the severe scenario, besides the mechanisms at play under the adverse scenario, the college free energy prices, along with a farther increase in spreads on fiscal markets, lead to significantly lower real Gdp growth compared with the baseline (-1.4 percentage points in 2022 and -0.five percentage points in 2023). In 2023, the more than persistent disruptions related to the war imply that the catch-upwardly furnishings on growth would exist limited, with growth 0.3 percentage points higher in 2024.

Tabular array

Alternative macroeconomic scenarios for the euro area

(almanac percentage changes)

Inflation would reach very high levels, on average, in 2022 nether both scenarios only decrease progressively thereafter to stand in 2024 below the baseline of 1.nine% in the adverse scenario and at the baseline level in the severe scenario (Tabular array and Chart B). Assumptions about energy prices are the ascendant commuter for HICP aggrandizement. The higher sensitivity of energy prices to supply cuts and the fewer offsetting factors nether the astringent scenario lead to a higher and more prolonged surge in HICP inflation. As such, the inflationary effects due to college commodity prices amount to 0.8 percentage points in 2022 in the adverse scenario and to 2.0 pct points in the astringent scenario. In 2023, the upward pressures persist in the severe scenario, with HICP aggrandizement 0.half-dozen percentage points higher than the baseline. As oil and gas markets rebalance, the big spikes in energy prices gradually unwind, leading, with weaker euro area action, to lower aggrandizement. In the severe scenario, more elevated free energy prices likewise as stronger second-round effects take HICP aggrandizement back to the baseline rate of i.ix% in 2024.

Chart B

Impact of alternative scenarios on real GDP growth and HICP inflation in the euro area compared with the baseline

(deviations from the March 2022 baseline projections, in percentage points)

Source: ECB staff calculations.

However, these scenarios abstract from a number of factors that may also influence the magnitude and the persistence of the impact. In detail, these scenarios have been prepared under the same financial assumptions as those of the March 2022 projections. As in 2021, governments may take action to cushion the impact of large energy prices hikes on consumers and firms. In addition, the estimated affect of gas supply interruptions on production does non consider commutation, which could atomic number 82 to an effect that is not as strong as assumed in the scenario. On the other mitt, an escalated and more protracted conflict entails the chance of a more pronounced and persistent impact. In add-on, likewise the free energy price hikes included in the scenarios, other commodity prices such as nutrient prices and some selected metal prices might too exist severely afflicted by the conflict given the role of Russian federation and Ukraine in global supplies of these commodities.

2 Fiscal outlook

Some further fiscal stimulus measures take been incorporated into the baseline since the December 2021 projections. After the stiff expansion in 2020, the euro area fiscal stance adjusted for NGEU grants is estimated to take tightened in 2021. This is mostly on account of revenue "windfalls" and other factors, which often manifest during a recovery. The fiscal stance is currently projected to tighten further in 2022, on account of the reversal of a meaning part of the pandemic emergency support, and to a much lesser extent over the rest of the projection horizon. Compared with the December 2021 projections, the financial stance is expected to exist around 0.ii percent points of GDP looser in 2022 and broadly unchanged over 2023-24. For 2022, the revisions reflect, amongst other things, additional stimulus measures adopted by governments in response to the Omicron moving ridge and new measures to compensate for higher energy prices, also every bit a partial reversal of acquirement windfalls from 2021. This boosted fiscal impulse is partly compensated for by more subdued growth in expenditure, specially regime consumption and transfers. Fiscal assumptions and projections are currently surrounded by a high degree of uncertainty related to the war in Ukraine, with the risks assessed to be tilted towards the introduction of additional stimulus.

The euro area upkeep residual is still projected to amend steadily in the period to 2024, but by less than foreseen in the December 2021 projections. The euro surface area budget arrears is estimated to take remained high in 2021, having peaked in 2020. Over the projection horizon the substantial improvement in the budget residue is seen to exist driven mainly past the cyclical component and the lower cyclically adjusted primary deficit. At the end of the horizon the budget balance is projected to be -2% of GDP and thus to remain below the pre-crisis level. Afterward the sharp increase in 2020, euro area aggregate authorities debt is expected to decline over the entire projection horizon, reaching about 89% of GDP in 2024, which is above its pre-pandemic level. The decline is seen to be mainly due to favourable interest rate-growth differentials, but also to arrears-debt adjustments, which together more than offset the persisting, albeit decreasing, primary deficits. Compared with the December 2021 projections, the estimated upkeep remainder outcome for 2021 has been revised significantly upward, reflecting both a higher revenue-to-Gross domestic product ratio and a lower expenditure-to-GDP ratio. Despite the higher starting point, the budget balance in 2024 is now projected to be lower than foreseen in Dec, following the deterioration in the macroeconomic outlook triggered by the state of war in Ukraine and the up revisions to interest payments as a share of Gross domestic product. The path of the euro area aggregate debt ratio has been revised downwards over the unabridged projection horizon, mainly on business relationship of favourable base of operations effects from 2021.

iii Prices and costs

Headline aggrandizement reached 5.eight% in Feb 2022 and is projected to remain elevated over the coming quarters (Chart three). Inflation is being driven mainly past energy inflation, which rose to around 32% in February, generally on business relationship of higher gas and electricity tariffs. These ii components are also expected to sustain energy inflation at high rates over the course of the year. By contrast, the contribution from fuels is expected to fade abroad in 2022 owing to base of operations effects and an assumed downward-sloping profile of oil prices. Electricity and gas tariffs recorded a large month-on-month increment in January, with prices being reset for the new year in many countries, and further increases are expected in the course of the year as the surge in wholesale gas futures prices caused past the war in Ukraine is gradually passed on to consumers (although base of operations effects imply some declines in almanac inflation rates later in the year). HICP inflation excluding energy and nutrient is expected to be 2.6% in 2022, owing to loftier need, indirect effects from higher free energy prices and cost pressures along the pricing chain related to supply bottlenecks. Food inflation increased to 4.ane% in February and is expected to remain high throughout 2022, attributable to loftier commodity prices and boggling increases in gas and electricity prices, which account for effectually xc% of the full free energy costs of the processed food industry and are an important factor for the production of fertilisers. Headline inflation is expected to turn down in the second half of the year on the back of large negative base of operations effects and an causeless downward-sloping contour of oil prices.

HICP inflation is expected to decline from an boilerplate of 5.i% in 2022 to ii.1% in 2023 and 1.9% in 2024. This decline in headline inflation over the projection horizon reflects sharp declines in energy inflation in line with the supposition that oil and gas prices will follow the downwards-sloping profile of their respective futures curves despite some upward impact from i) the reversal in 2023 of temporary fiscal measures to reduce energy prices, ii) national climate change measures in 2023-24, and iii) lagged effects of earlier potent increases in wholesale gas prices. Nutrient aggrandizement is also expected to decrease over the projection horizon. HICP inflation excluding free energy and food is projected to ease somewhat to stand up at i.eight% in 2023, and and then to increase to 1.9% in 2024. The initial easing results from the unwinding of upwardly impacts from supply bottlenecks as they are resolved and from the effects of the reopening of the economy, also as base effects. While the agin impact on growth from the war in Ukraine might have some dampening effects, these are probable to be beginning past indirect furnishings from the higher free energy prices triggered by the conflict. The slight increase in 2024 is in line with a tightening of product and labour markets, some second-round effects on wages from the inflation spike in 2021 and 2022, as well as longer-term inflation expectations being anchored at the ECB'south inflation target of 2%. The baseline projections are surrounded by meaning doubtfulness on business relationship of the war in Ukraine, peculiarly given the stiff further increases in energy prices since the underlying technical assumptions were finalised. The alternative scenarios presented in Box iii embed high free energy prices.

Growth in compensation per employee is projected to be 3.half dozen% in 2022 and to refuse to ii.nine% in 2024, remaining above the historical boilerplate recorded since 1999 (2.2%). Although compensation per employee, which was greatly distorted by policy measures in 2021, is envisaged to decrease somewhat, unit labour costs are expected to increase, driven by lower growth in productivity per person employed. The in a higher place average wage growth reflects the tightening labour marketplace, the expected increase in the minimum wage in Deutschland in October 2022 and some 2d-circular effects from the high rates of inflation.

Chart iii

Euro area HICP

(annual percentage changes)

Note: The vertical line indicates the start of the projection horizon.

External price pressures are expected to exist significantly stronger than domestic toll pressures in 2022 but to drop to considerably lower levels in the later on years of the project horizon. The almanac growth rate of the import deflator is expected to exist eight.ii% in 2022, largely reflecting increases in oil and non-energy article prices but also some increases in input costs related to supply shortages. As of 2023, import toll growth is expected to moderate and to stand at 0.7% in 2024.

Compared with the December 2021 projections, the outlook for HICP aggrandizement has been revised upwardly by 1.9 percentage points for 2022, 0.3 percentage points for 2023 and 0.1 percentage points for 2024. Three-quarters of the cumulative revision relates to the volatile energy and food components, while the remaining one-quarter relates to the projection for HICP inflation excluding energy and food. These revisions reflect recent upward data surprises, stronger and more than persistent upward pressures from energy prices (stemming from the disharmonize in Ukraine) and supply disruptions, and stronger wage growth, also related to the planned increase in the minimum wage in Germany. The upwards revision also took into account the recent return of survey-based indicators of medium-term aggrandizement expectations to levels consistent with the ECB'due south aggrandizement target. In the outer years of the projections, these effects more than offset the negative impact on inflation of a pregnant upward revision to the market place-based assumptions on interest rates and the negative demand-related effects of the conflict in Ukraine.

Box 4

Forecasts by other institutions

A number of forecasts for the euro area are bachelor from both international organisations and private sector institutions. Nevertheless, these forecasts are not directly comparable with 1 some other or with the ECB staff macroeconomic projections, as these were finalised at dissimilar points in time. Importantly, none of the comparator forecasts currently include the affect of the war in Ukraine. Additionally, these projections use different methods to derive assumptions for fiscal, financial and external variables, including oil and other commodity prices. Finally, at that place are differences in working solar day adjustment methods beyond dissimilar forecasts (run into the table).

Comparing of recent forecasts for euro surface area real GDP growth and HICP inflation

(annual percentage changes)

Sources: MJEconomics for the Euro Zone Barometer, 24 February 2022, data for 2024 are taken from the January 2022 survey; European Commission Winter 2022 Economical Forecast (Acting), x February 2022; Consensus Economics Forecasts, 10 February 2022, data for 2024 are taken from the Jan 2022 survey; ECB Survey of Professional Forecasters, for the first quarter of 2022, conducted between 7 and 13 January; IMF Earth Economic Outlook Update, 25 Jan 2022; OECD December 2021 Economic Outlook 110.

Notes: The ECB staff macroeconomic projections report working mean solar day-adjusted annual growth rates, whereas the European Commission and the IMF written report annual growth rates that are not adjusted for the number of working days per annum. Other forecasts do not specify whether they report working day-adapted or non-working twenty-four hour period-adjusted data. Historical data may differ from the latest Eurostat publications due to data releases after the cut-off date for the projections.

The March 2022 ECB staff projections are below those of other forecasters for growth in 2022, while for aggrandizement in 2022 they are well above other forecasts, owing to the inclusion of the impact of the conflict in Ukraine and more recent data. For the outer years of the horizon, the differences are more limited. Despite the down revision compared with the December 2021 Eurosystem staff projection for growth in 2022, the March 2022 ECB staff project is but slightly beneath other more recent projections for 2022 and is still somewhat above other forecasts for 2023. As regards aggrandizement, the ECB staff projection is far higher than the other forecasts for 2022 owing to the more recent cut-off date, which fabricated it possible to include the Feb 2022 HICP flash estimate and more than upwardly-to-engagement technical assumptions following the Russian invasion of Ukraine. For 2024, the ECB staff projections are within a much narrower range of other forecasts for both growth and inflation.

© European Central Bank, 2022

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and not-commercial purposes is permitted provided that the source is acknowledged.

For specific terminology please refer to the ECB glossary (bachelor in English only).

PDF ISSN 2529-4466, QB-CE-22-001-EN-North

HTML ISSN 2529-4466, QB-CE-22-001-EN-Q

Source: https://www.ecb.europa.eu/pub/projections/html/ecb.projections202203_ecbstaff~44f998dfd7.en.html

{kind=link}

Post a Comment for "What Is the Event in the Headline Most Likely a Response to?"